.jpg)

Published by Jacob I. Oberlander, CPA

Last Updated November 4, 2025

Do you occasionally have your teenage children or grandchildren helping you at the office on weekends, after school, or during their summer break? If so, you may want to consider putting them onto payroll. If you already have payroll set up for your company, adding your children should not be that big of a hassle. (However, if they just work once in a while, you might want to bypass the formalities and just add something to their allowance.)

In addition, there is the added benefit of teaching your children a good work ethic and understanding the value of money.

This article is for educational purposes and is not intended to provide legal advice. It is important to note that your individual circumstances may affect the information provided in this article. We recommend consulting a professional for personalized guidance.

Let’s review an example of the amount of potential tax savings;

- Income Tax

- Let’s take an example: your federal tax rate is 25%, and your state tax rate is 7% for a combined 32%.

- In comparison, if you hire your child/grandchild and do the accounting right, they will pay no federal income taxes on the first $15,750 earned in 2025. They will most likely pay very little state income tax, and even if they end up earning more, the federal and state tax rates will be relatively low.

- In this example, paying your child $15,750 saved you approximately $5,040 in income taxes.

- Kiddie Tax doesn’t apply to ‘earned income’

- But wait, there is more; you can save on social security and other taxes as well!

- If your business operates as a sole practitioner (also known as a schedule C), or if you and your spouse have a partnership (or an LLC taxed as a partnership) and employ your children, you may save even more taxes. If the kids are minors, you won’t need to pay, and the kids won’t need to pay Social Security, Medicare, or FUTA taxes on their wages. Social Security & Medicare is another 15.3%, so combined with the 32% savings, we’re up to a total savings of approximately $7,449.75!

.jpg?width=760&name=shutterstock_1692929905%20(1).jpg)

Here is the procedure: The IRS allows any sole proprietorship or partnership (LLC) that is wholly owned by a child’s parents to pay wages to children under age 18 without having to withhold the payroll taxes.

When your child performs the work, you will pay them as you would pay any employee and issue a W-2 for your child; there are no FICA, FUTA, or SUTA due or withheld. (In Alexander, Michael D. v. Comm. the court disallowed wages paid to kids under 18 because no W-2 was filed.)

Now that you understand the value of hiring your children, be sure to understand and comply with the following;

- The pay is reasonable and not excessive.

- Per the regulations, the amount paid must be reasonable for any wage to be deductible. To be on the safe side, make sure that you pay the going salary. Don’t pay more than you would to an unrelated party who would have filled the job. If you have never had anyone in that position, ask around. An excessive salary is sure to raise a red flag.

- Tip to play it safe: pay your kids the minimum wage.

- Ensure that the children are suitable for the job.

- Examples of jobs that are not suitable for kids – Fieldwork. State law requires anyone working in a dangerous industry to be at least 17, so if you run an auto mechanic shop, you can’t hire your 12-year-old to help you.

- Examples of suitable jobs – light office work. Your high school child can help you clean the office, stuff envelopes, do data entry, and light bookkeeping jobs. Etc.

- Set it up properly and keep records

- Make sure that the child has their own bank account in their name

- Keep in mind, if audited, the IRS is quick to investigate family members’ payroll. If it’s clearly not possible the child could have performed the work as claimed, the IRS will disallow the payments. Document everything. Keep a log of days and hours worked, what was done, etc.

- Child labor laws

- Federal Law - Children of any age are generally permitted to work for businesses entirely owned by their parents, except mining, manufacturing, and any other occupation the Secretary of Labor has declared to be hazardous.

- State Law - some states have age restrictions on top of the federal law, so check the specific labor laws in your state.

- Please check here the New York regulation regarding youth employment.

- Age

- The child must be age seven or older; however, in practical terms, your child will need to be around the age of 12 to do any meaningful work.

- Once your child is 18 years or older, they are no longer exempt, and you will need to pay them and deduct taxes the same as you would for your other employees.

- Roth IRA for Kids - By having your children on payroll, they can contribute to a Roth IRA tax-free.

.jpg?width=2868&height=2190&name=shutterstock_1802045431%20(1).jpg)

🚩 A few notes of caution

- If you have an S or a C Corporation, you do not receive this benefit of avoiding FICA when paying your children. Even if you are not able to save on paying social security, you still might save on taxes if you are in the higher than 15% bracket plus you can still do a Roth IRA.

If you do want to save on FICA taxes, the only way to pay your kids tax-free is through a sole proprietor’ management company.’ You do this by paying a legitimate management fee to the management company from the S-Corporation and then paying the children out of the sole partnership or single-member LLC. - Workers Comp

- In some states, including New York, you might be required to have your children covered.

- In some states, including New York, you might be required to have your children covered.

- Hiring Grandchildren, nieces, or nephews. While the IRS only allows hiring children, there is a possible workaround when paying grandkids through a parent-owned management company.

- State Filings Considerations:

- New York State (and possibly other states) have a special standard deduction amount for someone who can be claimed as a dependent on another taxpayer’s federal return. For 2025, the amount is $3,100

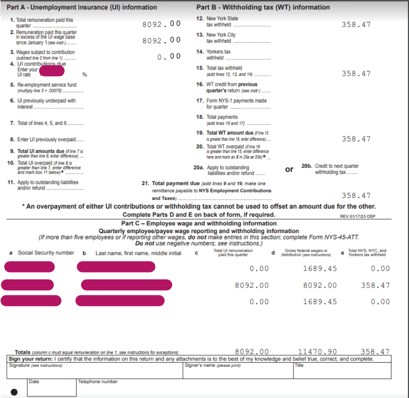

- New York State - Payments made by a sole proprietor to the sole proprietor, his or her spouse, or minor (under 21) child, and payments made by a partnership to the partners are excluded from remuneration. See the screenshot below.

We’ve made it simpler than in real life. Be sure to discuss this with your accountant if this may apply to you. Make sure to read the IRS website here and here to learn more. This article also covers this topic in-depth.